The EU Sustainability Reporting Standards (ESRS)

The European Union Sustainability Reporting Standards (ESRS) are an upcoming set of EU compliance and disclosure requirements first previewed by the European Commission and the European Financial Reporting Advisory Group (EFRAG) on May 3, 2022.

At its November 2022 meeting, the International Sustainability Standards Board (ISSB) voted to require the publication of sustainability reporting at the same time as financial reporting. The ESRS, a reporting framework under the Corporate Sustainability Reporting Directive (CSRD) is an amendment to the existing EU's Non-Financial Reporting Directive (NFRD), and will go into effect throughout the European Union in 2023:

· In 2023, organizations will need to track their environmental social governance (ESG) strategy, risks,and performance to prepare their ESRS reporting.

· In 2024, qualifying businesses will need to disclose a ESRS compliant report according to a first set of sustainability reporting standards for their 2024 financial year.

· In 2025, companies will repeat the same ESG reporting cycle for fiscal year 2025.

· In 2026, EU small and medium enterprises (SMEs) will need to start their own ESRS reporting using the follow-on, streamlined reporting system designed for small businesses.

The ESRS are designed to make corporate sustainability and ESG reporting within the EU more accurate, common, consistent, comparable,and standardized, just like financial accounting and reporting.Sustainability-related financial disclosures would also need to be authorized by the same bodies or individuals that authorize the financial statements(e.g., the full board).

The ESRS will apply to all companies with:

· Over 250 employees

· More than €40 million in annual revenue

· More than €20 million in total assets

· Publicly listed equities and have more than 10 employees or €20 million revenue

· International and non-EU companies with more than €150 million annual revenue within the EU and which have at least one subsidiary or branch in the EU exceeding certain thresholds.

Any EU company that meets those criteria is required to file an annual report using the final ESRS guidelines, including disclosure of how sustainability influences their business, as well as the company's impact on people and the environment.

To comply with ESRS, organizations will need to take the following annual compliance steps:

· Prepare and submit an ESRS report- A company's first ESRS report will be due in early 2025 based on the company's 2024 fiscal year environmental performance, with SMEs and international companies needing to comply in later years.

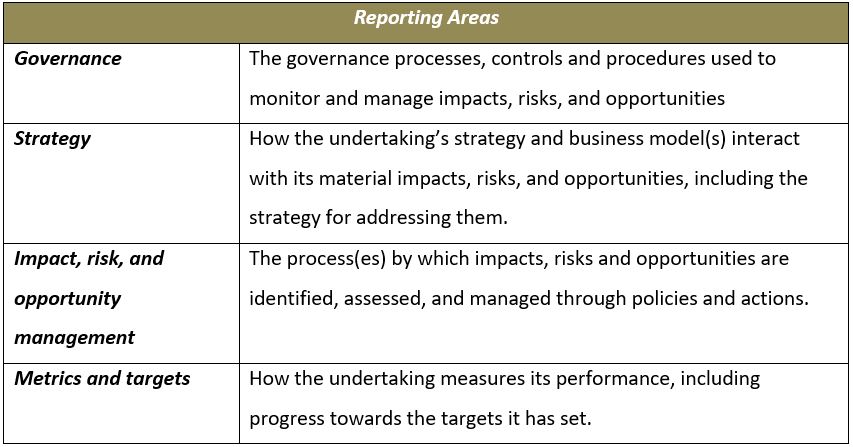

· Track and disclose the required information – Companies should disclose all material information on its sustainability-related impacts, risks, and opportunities in accordance with applicable ESRS. Applicable ESRS mandate reporting under standardized sector-agnostic and sector-specific disclosures. These disclosures are complemented by entity-specific disclosures. ESRS reports must cover ESG matters,including management commentary and data on a company's:

- Strategy and business model in relation to sustainability

- Governance and organization in relation to sustainability

- Materiality assessment process to select material ESG themes, topics, risks, and opportunities,including a description of the process to identify sustainability impacts,risks and opportunities and assess which ones are material

- Sustainability and ESG performance implementation measures, covering policies, targets, actions and action plans, and allocation of resources

- Performance metrics

· Digital data and tagging - Companies must prepare their financial statements and management statement in XHTML format in accordance with the ESEF regulations and the EU sustainability taxonomy, then digitally ‘tag' their reported sustainability information according to a digital categorization system specified by the ESRS Regulation (or use ESG software that can auto-tag and format data).

· Third party assurance - Organizations reporting under ESRS will also be required to seek "limited" assurance of the sustainability information they disclose from a neutral, trusted, and experienced third party who reviews the data. "Limited" assurance is less strict than a financial audit, but still requires working with a sustainability reporting partner organization.

Companies should report on four reporting areas, three reporting layers in three topics as noted below:

The ESRS are ambitious and would have a significant impact on the scope, volume, and granularity of sustainability-related information to be collected and disclosed by companies. Svarmi recommends making yourself familiar with the proposed reporting requirements under ESRS and identify what you would be required to report.

Companies should establish a board-led governance structure to identify impacts, risks and opportunities and perform a materiality assessment that covers not only the reporting company but also its upstream and downstream value chain. It is important to engage current process owners and understand how the information is being defined, captured, and reported and where is information not being captured. Systems, processes,and controls should identify relevant sources of content to meet disclosure requirements. ESRS will be a big initiative, it is time to plan early.